For weeks, the mortgage market has felt like a boat becalmed in the doldrums. The data, when you strip away the market chatter, paints a picture of frustrating stasis. We’ve seen fractional movements, sure, but nothing that signals a decisive shift. Homebuyers and those eyeing a refinance might have felt a glimmer of hope back in late August and early September when rates nudged downward. But that relief, much like a fleeting summer breeze, proved temporary.

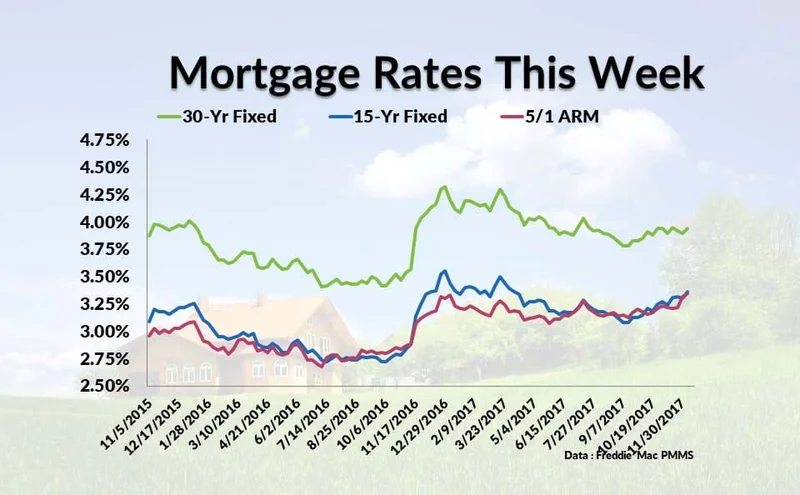

Look at the numbers. As of November 21, Optimal Blue data showed the average 30-year fixed-rate conforming mortgage ticking up to 6.244%—a single basis point higher than the day before, and five basis points above the prior week, as reported by Current mortgage rates report for Nov. 21, 2025: Rates mostly steady - Fortune. Two days later, Zillow’s national average put the 30-year fixed at 6.11%. By November 24, Optimal Blue had it at 6.236%, barely a twitch, a trend noted in Current mortgage rates report for Nov. 24, 2025: Rates appear to be in holding pattern - Fortune. This isn't a market making a move; it's a market holding its breath. The 30-year conventional rate, for example, has been hovering persistently around the low 6% range (specifically, 6.244% and 6.236% on those dates), a tight band that belies any real momentum.

The Federal Reserve, in its wisdom, has already cut rates twice this year—once in September and again at the end of October. There’s talk, strong talk, of a third cut coming in early December. Conventional wisdom, the kind you hear echoed in every financial pundit's monologue, suggests these cuts should translate to a more aggressive downward trend in mortgage rates. Yet, here we are, watching rates dance within a painfully narrow corridor. This is the part of the report that I find genuinely puzzling; the expected correlation between Fed action and market response appears to be operating on a delayed, or perhaps entirely different, timeline. It makes you wonder: if the Fed can't decisively move the needle, what forces are truly at play, and are we underestimating their grip?

The prevailing sentiment among many observers is that 30-year mortgage rates have been "stuck near 7% for an extended period." And while it’s true that rates did surpass 7% in January 2025, according to Freddie Mac, and lingered there for a spell, the current data shows a retreat. We’re not at 7% now; we’re firmly in the low 6s. This discrepancy between perceived reality and numerical fact highlights a crucial point: memory is a poor substitute for data. The disappointment that anticipated rate softening after the Fed's September 2024 cuts didn't lead to a sustained decrease has clearly colored the public's perception, making current rates feel higher than they are.

This sentiment is particularly acute for the "golden handcuffed" homeowners. They’re the ones who locked in those historic, almost absurdly low pandemic-era rates—think 2.65% in January 2021. For them, a 6% mortgage rate, even if it's trending down, feels like a financial prison sentence. And who can blame them? Moving means relinquishing a once-in-a-lifetime deal. But the historical context is vital here, and often forgotten in the heat of current frustration. Rates around 7% weren’t unusual from the 1970s through the 1990s. My analysis of the long-term charts shows that for significant stretches, rates above 10% were common, even hitting a staggering 18% in 1981. The ultra-low rates of recent memory were an anomaly, a product of unique circumstances—the Fed holding its key rate at zero post-Great Recession and unprecedented pandemic-era stimulus. To compare today's market to 2021 is to compare apples to an entirely different fruit, perhaps one from another planet. The 2-3% range? Experts widely agree we won't see that again in our lifetimes, short of another global catastrophe.

So, what's holding us in this current pattern? The usual suspects are still pulling the strings: the broader U.S. economy, persistent inflation fears, the national debt, and the ever-present demand for home loans. There's also the Fed's balance sheet management, subtly shrinking it by letting maturing assets roll off without replacement. Some observers are even throwing President Donald Trump's potential policies (tariffs, deportations) into the mix, speculating they could constrict the labor market and reignite inflation, further complicating the Fed's playbook. While the specifics of these future policies remain speculative, the anticipation alone can introduce a level of market uncertainty that limits aggressive rate movements.

For those still looking to buy or refinance, the advice remains stubbornly consistent because the underlying mechanics haven't changed. Your credit score is paramount (740+ for top tier, 620 minimum for conventional). Your debt-to-income ratio needs to be tight (aim for 36% or below). And crucially, you have to shop around. Freddie Mac’s research, based on hard numbers, suggests that comparing offers from multiple lenders—big banks, local credit unions, online outfits—could save you hundreds, even over a grand, annually. It's not glamorous, but it's where the numerical advantage lies. Don't just look at the interest rate; the Annual Percentage Rate (APR) is your true north, incorporating interest, discount points, and all those pesky fees.

The market isn't collapsing, nor is it soaring. It's in a standoff, a tug-of-war between the Fed's deliberate unwinding and the stubborn realities of inflation, demand, and a collective memory that's still fixated on a deeply abnormal period. The fractional movements we're seeing aren't signs of an impending breakthrough, but rather the subtle vibrations of a system trying to find its new equilibrium. Don't expect a dramatic drop anytime soon. The data clearly indicates we're settling into a new normal, one where the low 6s might just be the new 3s—not what anyone wants to hear, but it's what the numbers are telling us.